Featured

Table of Contents

The primary distinctions between a term life insurance policy and a long-term insurance plan (such as entire life or global life insurance policy) are the period of the policy, the accumulation of a money value, and the expense. The right option for you will depend upon your requirements. Here are some things to take into consideration.

Individuals that own entire life insurance pay more in costs for much less insurance coverage but have the security of recognizing they are shielded forever. Level term life insurance rates. People who acquire term life pay premiums for an extended duration, but they get nothing in return unless they have the tragedy to pass away before the term runs out

Substantial management fees typically reduced right into the rate of return. This is the source of the phrase, "get term and spend the distinction." The performance of irreversible insurance can be stable and it is tax-advantaged, providing added advantages when the stock market is unstable. There is no one-size-fits-all response to the term versus irreversible insurance debate.

The biker assures the right to convert an in-force term policyor one ready to expireto an irreversible strategy without experiencing underwriting or proving insurability. The conversion motorcyclist need to permit you to transform to any type of permanent plan the insurer provides with no constraints. The key attributes of the cyclist are keeping the original wellness ranking of the term plan upon conversion (even if you later have health concerns or become uninsurable) and determining when and just how much of the coverage to convert.

30-year Level Term Life Insurance

Certainly, overall costs will certainly increase dramatically considering that whole life insurance policy is more pricey than term life insurance policy. The advantage is the guaranteed authorization without a medical test. Clinical conditions that develop during the term life duration can not cause premiums to be increased. The firm might need minimal or full underwriting if you want to add extra riders to the new plan, such as a lasting treatment cyclist.

Entire life insurance coverage comes with significantly greater regular monthly premiums. It is suggested to give insurance coverage for as lengthy as you live.

It depends upon their age. Insurance provider established a maximum age restriction for term life insurance policies. This is usually 80 to 90 years of ages, yet might be greater or reduced depending upon the firm. The premium additionally increases with age, so a person aged 60 or 70 will certainly pay significantly even more than someone years more youthful.

Term life is somewhat comparable to automobile insurance policy. It's statistically not likely that you'll need it, and the costs are cash down the tubes if you do not. If the worst occurs, your household will get the advantages.

Where can I find Level Term Life Insurance For Young Adults?

___ Aon Insurance Coverage Providers is the brand name for the brokerage and program management procedures of Fondness Insurance coverage Providers, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Affinity Insurance Policy Company, Inc. (CA 0795465); in Alright, AIS Affinity Insurance Policy Providers Inc.; in CA, Aon Fondness Insurance Coverage Providers, Inc.

The Strategy Representative of the AICPA Insurance Count On, Aon Insurance Policy Services, is not associated with Prudential. Group Insurance protection is issued by The Prudential Insurance Policy Firm of America, a Prudential Financial firm, Newark, NJ.

For the many part, there are two kinds of life insurance coverage plans - either term or irreversible plans or some mix of the two. Life insurance providers supply different types of term plans and standard life policies along with "passion delicate" items which have come to be extra common since the 1980's.

Term insurance coverage supplies security for a given period of time - Level term life insurance policy. This period can be as short as one year or give protection for a specific number of years such as 5, 10, 20 years or to a specified age such as 80 or in many cases as much as the earliest age in the life insurance policy death tables

Fixed Rate Term Life Insurance

Currently term insurance prices are very competitive and amongst the most affordable historically skilled. It needs to be kept in mind that it is an extensively held belief that term insurance is the least pricey pure life insurance policy protection available. One requires to review the plan terms thoroughly to determine which term life options appropriate to meet your particular conditions.

With each new term the costs is boosted. The right to restore the policy without proof of insurability is a vital advantage to you. Or else, the threat you take is that your health and wellness might degrade and you may be not able to get a policy at the same rates and even whatsoever, leaving you and your recipients without coverage.

You have to exercise this option during the conversion duration. The size of the conversion duration will vary depending on the kind of term policy bought. If you convert within the prescribed duration, you are not called for to give any info concerning your wellness. The premium price you pay on conversion is usually based upon your "present achieved age", which is your age on the conversion day.

What is included in Level Term Life Insurance Policy coverage?

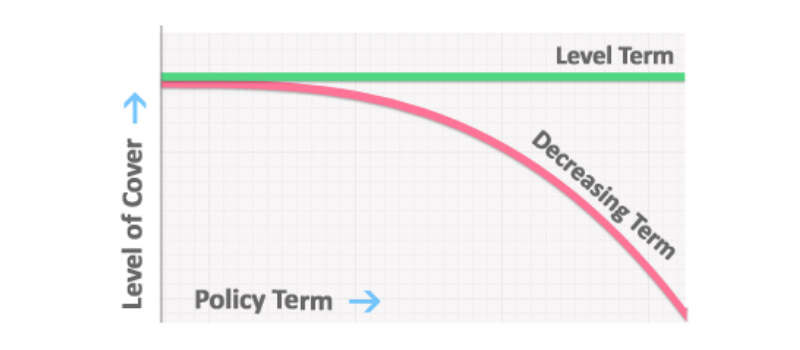

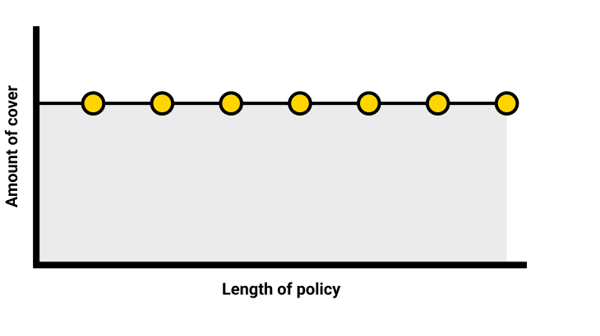

Under a level term policy the face amount of the plan stays the same for the entire period. With decreasing term the face quantity minimizes over the duration. The premium stays the same every year. Frequently such policies are marketed as home mortgage defense with the quantity of insurance coverage lowering as the equilibrium of the mortgage lowers.

Typically, insurance companies have not had the right to change premiums after the policy is sold. Since such plans may continue for several years, insurance companies must utilize conservative mortality, rate of interest and expense rate quotes in the premium calculation. Adjustable costs insurance policy, nonetheless, enables insurance companies to offer insurance coverage at lower "existing" premiums based upon much less traditional assumptions with the right to alter these premiums in the future.

While term insurance coverage is developed to offer protection for a defined period, permanent insurance is designed to offer protection for your entire life time. To maintain the premium rate level, the premium at the younger ages goes beyond the actual price of security. This additional costs develops a reserve (money value) which aids pay for the plan in later years as the cost of security increases above the costs.

What happens if I don’t have Level Term Life Insurance Companies?

With level term insurance policy, the cost of the insurance coverage will stay the very same (or potentially lower if returns are paid) over the term of your policy, normally 10 or twenty years. Unlike long-term life insurance coverage, which never ever runs out as lengthy as you pay premiums, a degree term life insurance policy plan will certainly finish at some factor in the future, normally at the end of the duration of your level term.

Due to this, numerous individuals utilize permanent insurance policy as a stable financial preparation tool that can serve several requirements. You may have the ability to convert some, or all, of your term insurance coverage during a collection period, typically the initial one decade of your policy, without requiring to re-qualify for coverage also if your health has actually changed.

Why is Low Cost Level Term Life Insurance important?

As it does, you might intend to include in your insurance coverage in the future. When you first obtain insurance policy, you may have little savings and a big home mortgage. Eventually, your financial savings will certainly expand and your mortgage will reduce. As this occurs, you might desire to ultimately minimize your survivor benefit or consider converting your term insurance coverage to a permanent policy.

Long as you pay your costs, you can rest easy understanding that your liked ones will certainly obtain a death advantage if you die during the term. Numerous term policies enable you the ability to transform to irreversible insurance policy without needing to take one more health and wellness test. This can allow you to capitalize on the extra advantages of a permanent policy.

{kind=link}

Latest Posts

Funeral & Final Expense Insurance

Instant Approval Life Insurance

Life Insurance Quotes Instant